|

||||||

|

美國聯儲局一句「經濟放緩風險顯著」,令「雙底衰退」憂慮重燃,更促成環球股災,港股周四(22日)更是傷亡慘重,縱使周五(23日)稍為收復失地,但壞

消息仍不絕,諸如穆迪下調8家希臘銀行的長期存款與高級債券評級兩個級別,前景展望全為「負面」;希臘財長維尼澤洛斯(Evangelos

Venizelos)更警告說希臘可能違約,國際貨幣基金組織(IMF)前首席經濟師羅格夫(Kenneth

Rogoff)更表示,歐元區最大風險是南歐銀行擠提。亞洲亦好不了多少,7間南韓儲蓄銀行因周轉資金不足,被迫停業半年…… 歐美債務接連出現壞消息,令港股1周跌近1,800點,還未計及以上利淡消息接踵而至,若只計8月至今,恒指已下跌了4,770點,還會繼續跌嗎?愈跌愈 買的散戶都心死了,後市真的如此差勁嗎?Look's Asset Management Limited董事總經理兼投資總監陸東說,當港股跌至17000點時,第一步是考慮增持。然而瑞信亞洲區首席經濟分析員陶冬則認為,希臘爆煲及資金流出 新興市場等問題不容忽視。 陸東論勢 香港股市篇 恒指未跌完還有終極一跌 歐、美債務危機折騰了港股兩個月,8月至周五短短一個多月,港股最多跌5,000點,單是9月至今跌幅亦達13.9%,周四一天恒指都跌912點。問題 是,股市未有止跌迹象。美國聯儲局的「扭曲操作」(Operation Twist)雖然距離我們很遠,但港股跌幅竟較美股深,打擊了環球股市之餘更傷盡了股民心。試問在人心如此虛怯下,還有誰敢在風雨飄搖下入市? Look's Asset Management Limited董事總經理兼投資總監陸東說:「敢!」他透露,當恒指跌至17000點時會考慮增持。他更堅信近5,000點的跌幅,只是「牛二」的調整,等待「終極一跌」後他就會積極入市。 跌破支持位將直撲萬七關 沒聽錯吧!「大好友」陸東竟然轉?,說要等「終極一跌」?絕對沒花假,陸東說:「我觀察中、港股25年,發現恒指有自己的性格,以前沒有中資股,恒指波動 沒那麼大,但由1993年青島啤酒(00168)上市開始,波動愈來愈大。據觀察所得,恒指一旦跌破支持位或者升穿阻力位,通常有10%上下波幅,是次港 股跌破8月初的18868點支持位,一般來說仍會下跌10%,即會落到17000點(編按:若以周四17912點計,若跌10%,港股將見16982 點)。」 在他眼中,恒指有機會進一步下跌,原因為何?他說:「可能一間金融機構疑似或者謠傳反肚,便會出現很多Counterparty Risk(交易對手風險);如果銀行A疑似或傳言反肚,大家會擔心與她有交易的銀行受多大影響,這樣就會在短短的一個交易時段出現好大跌幅。其實2008 年出現過,當時Bear Stearns(貝爾斯登)出事沒人理,接?就是雷曼,然後是Citibank、AIG,恒指就從20000點跌至10676點;若今次出現『終極一 跌』,我覺得是重複以前的路。」 一旦跌穿17000點,會再大幅下調嗎?他回應:「如果跌穿17000點,那時又有幾千億成交的話,當然會進一步下跌,但現在請不要來問我,跌穿了再算。若你問我,現在港股估值是否便宜?是否該撈底?我可以告訴你,現在港股估值好平。」 「問題是我覺得好平又如何,雖然我是價值投資者,但是今天股市已經不再是平與貴的問題。我慣用盈利收益率差模型(Earnings Yield Gap Model)來計算恒指合理值,該模型要看3個條件:債息、股市盈利及風險溢價(Equity Risk Premium),當中風險溢價最重要。股民們要問問自己,可承受多少風險。」 無人借錢「扭曲操作」徒然 他解釋︰「周四港股之所以跌912點,是因為萬眾期待一連兩天的議息會有好消息公布,憧憬聯儲局主席伯南克會有一個終極的拯救方案,不單只救美國,還能救 全世界。但經過兩日議息,竟然有人投反對票,加上所公布的『扭曲操作』沒有新意,不外乎買多些長債,令Yield(長債孳息)低些,這方法已經在過去3年 證明沒有用。因為今日的問題不在於息高與低,而在於投資者或是消費者還有沒有能力借錢,無論息口是10厘、1厘、0都好,都沒能力借錢了。」 「現在美國的問題是,要用時間去修復資產負債表,不是便宜就借多一些,再平都是借不到的,不是不想借,是沒人借。我懷疑這條藥方,市場已經不再相信了,現在就是患Cancer卻去吃止痛藥,如果不做手術,我不相信美國經濟可復甦。」 深信美國經濟將步入通縮 他一直相信,美國經濟不可能在短時間內復甦,當伯南克推出「扭曲操作」後,他更堅信,美國經濟問題更難解決。他說:「我一直不相信美國經濟會有復甦,好簡 單,美國人過去30、40年,整整四代人使錢使大了,無可能只是靠減息、印銀紙去解決問題,如果可以的話,這個世界就無窮人,印銀紙就得!」 「再看看國家及家庭負債相對於GDP為3倍,即是1元經濟實力有3元負債,已借爆倉,如何復甦?撇除一次過軍事定單,美國實質通脹其實在跌,如果你在圖上 畫一條直綫,已經看到通縮了,當然世界並不是畫一條綫咁簡單,但總的來說,趨勢是向下的。美國絕對沒有必要加息,伯南克話到明2013年息口仍會好低,我 可以話俾你聽,到2015年息口都仲係低。美國正在走日本1990年的舊路,非常之緩慢的增長,每次復甦都是反彈,回落以至衰退。」 「所以除了偉大祖國外,我不相信這個世界會有通脹。中國好明顯有通脹,但美國呢,我認為未來只有通縮無通脹。讀大學時有條公式MV=PQ,意思是,通脹的 成因除了銀紙多寡外,其他就是銀紙流轉的速度,今天可見流轉速度大幅減漫,因為沒人肯借錢,美國人已經借爆?,我懷疑美國未來幾個月會見通縮。若出現通縮 就會好慘,我們也捱過董建華(前特首)那68個月通縮期,資產價格大跌,入息跌但債務唔跌,好慘,供樓愈供愈辛苦。」 8大買平貨投資心法 陸東說,自己的投資理念很簡單,就是「買平?」。「不單要買平?,還要找到由平變成合理價值的契機,譬如2003年本地地產股,有了自由行,在中國幫香港這契機下,自然要買本地地產股,想都不用想。」 至於如何「揀平?」,陸東透露了8大步驟。他說:「一、要在1,500家上市公司裏揀一些便宜的公司。二、用不同的Financial Model代入公司。三、將所計算的數值與同行相比,例如大摩說這家公司睇5元,但我計來計去,都睇10元,我會反覆看,為何我會睇得多個佢呢?我並不是 說自己一定準,但要反覆求證。四、找出原因,點解人?覺得佢睇5元而我堅信係10元,差別在哪裏?可能大摩對盈利的估計過分保守,或是我低估資金成本,總 之一定要找出原因。」 「五、就算證明我是對,還要看Upside(上行)同Downside(下行)的風險。人家睇5元而我看10元,估價是3元,望上去有7元賺,望落去有幾 多?我們幫人管錢,一定要先封蝕本門,最緊要不要輸錢。究竟我3元買落去,上唔上到5元、10元。望落去1元,零元定係2.5元,這點好重要。」 投資理念︰絕不大出大入 「六、做盡職審查(Due Diligence),不可能不去見公司管理層,舉例說,我揀中新鴻基地產(00016),我不單只看新地,還要同時看信和置業(00083)、長江實業 (00001)、新世界發展(00017)等。七、Make Sure整個行業話我知,新地真係好正。八、最後落實投資。每一隻股票的買入,沽空或者沽出,我都要經過以上8個嚴謹步驟。」 他最後說:「我覺得我的風險評估做得非常好,一間公司值多少錢可以好好掌握,但有一件事,我做得非常差,就是對增長動力的估計。在過去25年的職業生涯 裏,我未見過一個人長期炒出、炒入可以賺大錢,可能他賺3鋪輸1鋪,輸就輸好盡。我的投資理念就是:不會大出、大入。」 投資揀股篇 3板塊可現價買入長? 縱使眼前面對很大風險,那股市就沒有上升的契機嗎?他說當政策穩定下來,加上大家發現中國企業的盈利增長動力猶在,股市自然會上升。他說:「股市仍然有上 升動力,皆因我們有偉大祖國關照。祖國是世界唯一一個每年增長8%以上的經濟實體,在此大前提下,全世界資金都會湧來香港,來港撞中國這道大門,令香港錢 好多。」 所以他堅信,在企業盈利增長仍得以維持下,港股在「終極一跌」後仍會回升。他說:「過去兩個月,我們看到40%以上的公司盈利符合預期,30%以上比預期 好,20%比預期差,例如思捷(00330),大部分主流上市公司如新地,過去25年來,好少見到她只有11、12倍PE、3厘幾息。」 新地長實盈利能力無憂 陸東說:「今日在芸芸資產投資中,投資股票的值博率最高,高過樓市好多。你買樓投資得3厘息,扣差餉、管理費、律師費,釐印費都3.75厘,買股票就不用支付這些開支,亂掟飛鏢買隻藍籌股息都4厘。今日,因為太平了,所以我仍然建議買入新地、長實這兩隻地產股。」 舉新地為例,他說:「今天新地確是好便宜,加上在香港做地產生意好好賺,全世界做地產都是『量』的生意,而香港則是『價』的生意。你們看,新地賣400多 億元物業,賺了150億元,好過賣白粉。一座凱旋門稅前盈利已經100億元。長實亦一樣,你將和記黃埔(00013)的市值從長實中抽出來,今日長實的資 產淨值,反映了地價跌一半,有無可能?將軍澳跌到去3,000蚊?有無可能?」 9月17日,陸東出席由新鴻基投資舉行的「大中華房產及股票部署策略前瞻」講座,在會上,他說看好基建、消費及澳門概念3大類板塊。 基建強勁看好中聯重科 他說:「如果你仍然相信中國基建投資好強勁,就應該買多些與基建相關的股份。我個人好鍾意中聯重科(01157),好平,1倍市帳率,10倍PE都無,20%的盈利增長。」 此外,在中國仍力谷內需下,他認為內需股中的國美電器(00493)很好又便宜。他說:「今後數年,消費概念類股份仍應在考慮之列,國美因有好好的分銷平台,以前股東們打架,但現在有一個輸了,打完架後可以睇返基本因素,仍是一間不錯的公司。」 他續說:「國內同胞來港自由行的數目一直在增加,內地遊客人均消費3,000多元,本地零售股股價最近回落了不少,由非常貴跌下來。我有意買入,現在仍在研究中。另外,澳門股亦不錯,當中我看好金沙中國(01928)有新賭場開,預期市佔率會增大。」 內銀股跌勢無損吸引力 陸東的粉絲都知道他對建設銀行(00939)、招商銀行(03968)情有獨鍾,但跟隨他入市的股民們相信不少已中伏,問他如何看內銀股?他說:「現在內 銀股平到好似『喊冷』咁,何解咁平?因為好多負面消息,一要融資,二是地方債問題,只要經濟維持增長,我不相信地方債的問題會很大。從另一個角度看,如果 你用有風險的資產相對ROE(股本回報率),內銀股是平,尤其是建行同中國銀行(03988),因為內地加了幾次息,Net Interest Margin上升,利潤有改善,以及撥備充足,我認為內銀不會出問題。」 「我每次到中國,官員都會問,有何方法令中國可以避免陷入日本式衰退?我的答案是,要維持一個穩健的銀行體系。日本捱了20年都無起色,因為銀行不行,如果中國的銀行可以維持一個非常穩健的財政狀況,我不相信中國的調整會好痛苦。」 香港樓市篇 堅信香港樓價跌不下 陸東過去那麼多年來,一直勸香港人要買樓,即使對港股轉口風,但對樓市的看法依然貫徹始終。他說:「早前與金管局前總裁任志剛吃飯,我很認同他一句說話, 他說:『你在香港做?、搵錢,人住在香港,你就是認同香港有增長的前景,你如果不擁有自己層樓,就是沽空香港。你信香港有增長又不信香港樓市,這是自相矛 盾的。』他說得很對,我很同意。如果你是自住,即使現在香港樓價已經好貴,但仍應該擁有一層樓。」 縱使今天的樓價確很貴,但他堅持香港樓價無得跌,他說:「樓會繼續貴落去,你看,未來幾年供應非常少,每季只拿5,000至6,000個單位出來賣,這只 屬杯水車薪。點解我話少,你看董建華那6年,1998年至2003年,每4個人就有1個負資產,8個人有一個失業,實質利率去到2、3厘,我們每年都吸納 2.5萬個單位,你現在話俾我聽息口係零,按揭息兩厘多些,中國增長8%以上,香港全民就業,得1萬個單位供應?實『夾爆』你啦。」 最大風險乃內地利息回升 陸東在《繼續傲行》一書中,亦提及在現時低息環境及全民就業下,樓價難以爆煲,「現時供樓負擔對家庭平均收入的比例(Mortgage to Average Household Income Ratio)現時才不過30%、40%,供樓非常舒服,1997年時則達100%;而且1997年按揭總額相對GDP為3.5倍,現時則只是2.1倍,相 當安全。」 不過陸東預示了樓價隱性風險,就是內地利息回升的風險。「如果來港買樓的內地人100%都是靠借錢,而他們的按揭都是在中國借的,內地銀行一收緊信貸便會出事。」 新書速遞「發達在於思想」 陸東於2009年1月出版新書《智者傲行》,事隔2年,他再推新書《繼續傲行》,新書主要分3大章,包括論身、論港及論天下。 「論身篇」除透露正全力支持兩大慈善機構:聖雅各福群會及小額借貸平台「我開」外,更披露另一志願為:「到監倉教書。」不說不知,原來他已立下平安紙,死後將全部身家、財產盡捐,他深信「他朝過世了,人在天堂、錢在銀行、毫無意義」,所以他全力支持這兩個機構。 他在「論港篇」中預言,有朝一日銀行可以在港借出人仔,而貸款利率並非由人民銀行控制,此則為「大茶飯」,他相信有朝一日終可實現。另外,他慨歎︰「香港的政治已經走入死胡同,沒得救,議會政治似乎是博上鏡,多過真心為市民服務。」 論「天下篇」方面,他預計,在不久的將來,港股直通車會真正出現,在可控制的範圍下,讓資金離開中國。篇章中較為特別的觀點是,他深信打工未必無發達的一 天,原來發達在於思想!他說:「我捱到金睛火眼,上北京一日開十個八個會,只睡兩、三個小時,但不知幾開心,因為我在做自己喜歡做的事,只要在做自己喜歡 的事,全情投入,做到全行最好,我擔保一定會發達。」 | ||||||

2011年9月29日 星期四

陸東親述暴瀉後最新部署

陶冬論勢 外圍經濟篇 最大憂慮乃美經濟已放緩

陶冬論勢

外圍經濟篇 最大憂慮乃美經濟已放緩

在9月20、21日召開的美國聯儲局公開市場委員會(FOMC)上,儲局主席伯南克宣布推出「扭曲操作」,即「買長沽短」的置換國債決定,加上聲明稱經濟

下行風險顯著,市場憂慮措施不足以提振經濟,拖累亞太區股市全?下挫。加上?豐(00005)公布的9月中國PMI從8月份的49.9顯著下降至

49.4,為繼8月份意外回升後重拾跌勢,引發市場對於中國經濟前景的擔憂;同時,外圍對全球經濟衰退憂慮擴散,令投資者信心頓失。在投資風險與日俱增

下,投資者該如何自處?

過去兩個月,港股跌了近5,000點,都說美國主權債務評級被降是罪魁禍首,

瑞信董事總經理兼亞洲區首席經濟分析員陶冬接受訪問時表示:「我認為,8月份股市下跌,並非標普降級美債所致。評級機構與政府債務的關係,相當於美食家和

餐廳的關係。美食家可能對於餐廳的客流量或有少少影響,但不會影響到這家餐廳的食品、服務的素質。評級機構是鏡子,不會對主體產生甚?影響。更具有諷刺意

義的是,美債被降級後,美國債市走出了一個近年罕見的牛市。」

所以陶冬堅信,美國不存在債務危機,因為美元是儲備貨幣,山姆大叔沒有錢還的時候,可印錢,問題是,它還值多少錢。現時美國的問題是經濟增長放緩,因此並

不存在甚麼美債爆煲。他說:「現時美國經濟需要的,並非為經濟強行注入興奮劑;相反量化寬鬆造成人們對經濟不切實際地樂觀。」這與實體經濟復甦之間出現落

差,這落差才是引發股災的罪魁禍首。他強調:「量化寬鬆令熱錢流入新興市場,一旦資金撤出,新興市場將有危機。」

美復甦受樓市及就業拖累

他認為,若撇除其他因素單獨看美國經濟,美國經濟實際上較去年好,所以縱使當前環球風險像是每日俱增,但他並不是對美國沒有信心。他說:「美國中小企業今

年請人的數字較去年多,銀行貸款也從負數進入正增長。只是經濟改善慢過歷史上其他多次衰退,在百年一遇的大危機過後,復甦很難強勁!」

他分析指,美國復甦主要受兩大市場疲軟所拖累,分別是房地產及就業市場。陶冬說:「首先,銀行業遭到重創,不借錢出來,作為經濟砥柱的房地產無法復甦,那

麼,經濟其他部分復甦一定非常緩慢。第二、就業市場方面,實際上商業、金融業、零售、醫療?生都在復甦。沒復甦的是製造業及建築業的就業,因為製造業的後

面是汽車業,建築業後面是房地產業,兩者皆屬結構性問題,我認為,即使推QE3也難真正解決問題。」

問題是,政治家們卻早已失去了等待經濟緩慢自然復甦的耐心。他說:「全球政府搞了一輪財政刺激,都負債纍纍。然後所有的央行都推出量化寬鬆政策,如果

QE1是為拯救金融業,QE2則是不折不扣的興奮劑。治標不治本,QE2注定失敗,其所不能夠拯救的是就業問題;若推QE3,相信亦都束手無策。短期內,

美國失業率或可從9%回落到8%,但回落到7%至6%的可能性極低。」

意大利可自救希臘定爆煲

陶冬坦言,相較美國的緩慢復甦,歐洲的問題更加嚴重。周二(20日),標普調低意大利主權評級,再度引發市場對歐元區骨牌效應的擔心。他回應說:「歐債問

題,短期是無法解決的,每隔3、4年就會出現階段性震盪。」歐洲最終是不會發歐債救希臘,因為會將德國、法國等大國主權信用與希臘綁在一起,所以歐洲打救

希臘可說是三心兩意。「希臘恐怕沒有能力靠自身之力,從債務絕境中解脫出來,違約只是時間問題。但是為?自身的利益和歐元的穩定,歐洲領袖對希臘不得不

救,至少要拖到其他歐豬的債務情?有所好轉。」

陶冬續指:「希臘最終一定會違約。歐洲整體債務水平低於美國,但其短板效應非常明顯。木桶的水容量取決於最短的那塊板——希臘。希臘兩年期國債利息超過80%,已然無力償還,大國貼錢也貼進無底洞,違約只是時間問題。」

但他認為,意大利則有能力自救。他說:「意大利問題在於增長,若其增長速度快過債務的積累速度,淨債務降低仍可自救。」他認為︰「意大利債務成本一定要壓在4%以下,中期才可能令GDP增長,加上通脹也維持在4%上下,希望稅收也跟隨經濟一起增長。」

他指摘歐洲領袖在這場危機中表現出「極具創意的愚蠢」,「原本可以以500億歐元救活的希臘,現在卻傳染到第二、第三個爛蘋果。意大利債務有1.5萬億歐元,如果再出事,歐債問題就沒得救。」

除了希臘會違約被踢出歐元區外,歐債危機仍有另外兩種可能:歐元區解體,或歐洲銀行危機。「德國、法國等或一起退出歐元區,長遠歐元區解體無可避免,但5

到10年之後才會發生。殺傷力最大的另一種可能,是出現一個違約後,歐債危機演變成歐洲銀行危機。」他認為,這或重演雷曼倒閉事件。雖然歐債數量遠超過雷

曼,但銀行體系和市場槓桿沒雷曼高,預計其爆炸力及全球災難影響力不及雷曼。

量化寬鬆釀新興市場危機

陶冬指,對經濟復甦無補於事的QE2,把市場價格炒上去了。他說:「人為的製造出債市的牛市,令10年期美債利息跌破2厘。資金成本低令各種勢力增加槓桿

去買風險資產,催生商品、股市的牛市。接?,股市暴跌,經濟復甦本來就緩慢,但市場在QE2之下,卻出現了不切實際的樂觀。」現時,在美國復甦緩慢,歐洲

又問題不斷,資金流向何方?他給出答案——新興市場。

「美國製造出那麼多的流動性,其銀行中介功能又壞死,令資金只能流入國債市場及新興市場。加上美國歐洲都在去槓桿化(Deleverage),熱錢早已流入新興市場。」

他解釋︰「無論2009年中國的財政4萬億元人民幣,還是現在的民間高利貸,或者是印度拼命的進行基礎設施投資,以及當下巴西海邊上比美國還貴的小屋,都是新興市場流動性增加的體現。」

如果說早前股市的暴跌可以被看做前車之鑑,那麼新興市場的蓬勃是否也只是危機前的短暫光明?他以九十年代初的日本舉例,指日本將大量流動性帶到東南亞投資

基礎設施。當日資撤出,就造成了1997年的亞洲金融危機。他提醒:「這場危機起於美國的槓桿爆煲,接下來是歐洲,最後是新興市場。今天新興市場的流動性

愈高,美國聯儲局退出的時候,就摔得愈重。」

中國篇 內地經濟數年內「慢增長」

瑞信剛調低了中國今明兩年的經濟增長預測,由8.7%和8.5%降至8.6%和8.2%,由下調幅度看,明年經濟似乎並不樂觀,但陶冬重申不是看淡中國經

濟,相比其他國家,中國經濟增速仍在前列。他說:「事實上,中國的投資和工業生產在放緩,但由於工資上升和減稅措施,令消費繼續擴張。雖然消費不能讓經濟

回復雙位數增長,若看按年趨勢,中國經濟增長將介乎8.5%至8.8%,中央領導人關注的月度數字,當中零售數據令人鼓舞,工業生產放慢,但看來仍相當穩

健,固定投資增速減少,仍有20%增長,哪裏有危機?」

金融中介功能嚴重弱化

他認為,中國經濟最大的問題,不再是通脹,甚至不再是增長放緩,而是銀行體系的金融中介功能嚴重弱化和經濟的去實業化,在這種情況下,即使貨幣政策出現放

鬆,經濟也很難回到雙位數增長。他的錦囊是「不要預言通脹何時見頂、不要預言經濟何時觸底、不要預言貨幣政策何時放鬆」。

他指,中國經歷了幾年高速增長,經濟正步入「慢增長」周期,根據過往經驗,慢增長周期往往歷時數年之久。從七十年代至今的經濟周期圖(見右頁圖),可見中

國先後出現3次強勁增長周期,其經濟增長均達10%以上,且歷時5至6年;值得注意是,3次強勁增長背景後都有一些利好因素支持。以七十年代的周期為例,

主要受惠於農村改革和鄉鎮企業的崛起,而上一次周期則因中國加入世貿和房地產興旺所致。

不過經濟高速增長後,通常有一段放緩時期,經濟增長回落至10%以下,他叫這段時間做「慢增長」周期。「現階段我看不到任何新的利好因素,其實每次超級增

長中間,都有一段回落期,歷時不是幾個月,而是幾年,通常伴隨?經濟的轉型,我覺得現時正處於其中一個經濟轉型期。」他說。

陶冬指,由於過往貨幣政策側重調高存款準備金率,一定程度已經對銀行體系帶來一些扭曲,令銀行體系的資金相當緊張,相反銀行外的流動性卻得不到控制,同時市場利率完全跟政策利率脫節,故造成了金融業的亂象。

「許多人說,現在中國貨幣政策很緊,真的嗎?假設雷曼倒閉前是處於一個正常水平,新增貸款和貨幣供應佔GDP(國內生產總值)比重,今年上半年的數字都高

於雷曼倒閉前的水平,真的很緊嗎?今天的息口也明顯低於雷曼倒閉前;只有存款準備金率和銀行同業拆息較高,這反映出銀行體系內的資金緊絀,但當你走出銀

行,社會充斥?投機的資金。」

瑞信數據顯示,中國今年上半年廣義貨幣供應(M2)佔GDP比重為182.1%,雷曼倒閉前為152.7%,而1年期貸款利率,今年6月為6.31%,雷曼倒閉前則為7.47%。為何外界感覺市場如此「水緊」?

企業寧願放貸不務正業

陶冬指,由於銀行的金融中介功能弱化,導致銀行體系內的資金周轉速度和效率下降,資金亦無法通過銀行有效配置到實質經濟。

「當有100元儲入銀行,當中便有20%被鎖進央行的準備金帳戶,不能動;第二個20%借給了地方政府,第三個20%注入了信託基金,由於央行限制貸款額

度,所以銀行以投資名義進入房地產項目,資金又鎖死了,動彈不得,銀行再將第四個20%借給大型國企,但國企並沒有很多新投資項目,國企把錢留在帳戶,只

有最後的20%存款由銀行支配。若一個人的肺部失去五分四功能,他又可以跑得多快呢?這正是銀行今天存在的問題,銀行的中介人功能在減弱,結果實體經濟相

當缺水,但投機的資金卻不缺。」

其次是經濟的去實業化,不單民企不再投資實業,連坐擁巨資的國企,寧可從事放貸業務,也不投資本業,結果形成產業空洞化,令實體經濟與金融經濟間失衡。

「2010年民企都不投資了,企業家都成了創投基金的投資者;2011年不僅民企不投資,國企也不投資了,國企全去放高利貸了,這種經濟的去實業化,以至

銀行金融中介功能的喪失,令中國經濟短期內難以出現強勁反彈。」

雖然歐美經濟並不明朗,中國本身亦存在一些結構性問題,但他看不到中國有硬?陸的機會,正如他說的「不要預言貨幣政策何時轉鬆」,反而貨幣環境正常化才是未來若干年的主調,包括調高利率和?率,並收回過剩的流動性。

內地通脹已於6.5%見頂

他說:「除非經濟出現急速惡化,經濟增長跌至6%以下,就業問題導致社會不穩定,否則不覺得今年的貨幣政策會放鬆,或有財政刺激措施出台。中央會接受經濟

增長在7%,通脹在5%以下,但若通脹在5%以上,試問貨幣政策怎會改變?我覺得內地通脹在6.5%已見頂,這是因去年的基數效應,你看豬肉和蔬菜價格按

月還在上升,工資上升的預期同樣增加,我的看法是,這個周期的頂部在6.5%,但通脹很大機會維持在5%至6%的水平,對人行來說,這不是好消息,因為利

率上調了,通脹卻未見回落,進行利息正常化仍有很長一段日子。」

他預計未來3至5年利率正常化事在必行,人行將加息150點子;換言之,1年期存款利率會由3.5厘升至5厘。

陶冬並不預測股市走勢,按他的說法,貨幣政策已連續擴張了8年,2011年僅是收縮的開始,瑞信預測中國今明兩年的M2增長將逐年減少,分別為16.2%

和15%。值得注意是,一向以來M2增長跟A股的關連性頗高,好像2004年至2007年中國M2增長便由14.6%增至16.7%,期間A股展開漫長升

浪;2009年M2更有27.6%的增長,當年A股升逾80%,然而2010年增速降至19.7%,股市馬上表現不濟,成了區內最差的股市;換言之,貨幣

環境正常化很有可能不利A股,以至港股的表現。

中國股市難有表現,樓市又怎樣?中國樓價高踞不下,皆因流動性過剩和利率偏低,讓內地居民不得不謀資金出路,買樓成了保值手段。陶冬指,當貨幣政策回歸常態,連溫州商人和山西煤老闆開始手緊時,中國樓價將難逃一跌,只是下跌速度會較緩慢。

內房約有15%下調空間

他解釋︰「目前住宅庫存相當於11個月的銷售量,我相信今年底還會升至15個月,接近2008年的水平,但問題是,現時的槓桿水平遠低於當時,大型發展商已透過發債、申請上市或配售股份集資,她們雖遇到資金緊張,但未到絕望的地步。」

他預計,被視為傳統旺季的「金九銀十」,發展商會將減價促銷,令成交量有輕微增加,但並不代表樓市調整已結束。「中國樓價有10%至15%的下調空間,我不相信未來12個月樓價會出現大幅度調整,長?來說,樓價會有顯著回落,但不是現在。」他說。

香港樓市已見頂

上周五,?豐宣布自周一起,其H按利率提升至H加2.3厘至2.7厘,隨後中銀、花旗等一眾銀行皆有提升按揭利率的舉動。早在今年6月,已撰文表示︰「不

買樓了。」的陶冬,仍保持自己的觀點。他認為:「6月?豐大幅上調H按利率,已是香港樓市由盛至衰的分水嶺。這次再加,暫時租金回報仍好過按揭成本。但在

銀行有其他放貸渠道、風險意識亦有所加強下,按揭利率會進一步上漲。不排除仍或有小陽春,但香港樓市已見頂。」在香港通脹無法放緩,持續負利率的情況下,

樓市短期不會大跌,卻如溫水煮青蛙,會慢慢跌,直到青蛙死掉。「當中國流動性逐漸正常化,內地房價出現大規模調整,加上美國的流動性退出時。3、5年後,

香港房價會有一次大幅度調整。」

2011年9月28日 星期三

传再裁员7000人 比亚迪瘦身错过最佳时机

传再裁员7000人 比亚迪瘦身错过最佳时机

比亚迪高层对记者坦言,比亚迪的“瘦身”错过了最佳时机

羊城晚报讯

记者孟庆利报道:比亚迪再次传出要大幅裁员的消息。据《中国经营报》消息,继不久前比亚迪汽车销售公司大幅裁员之后,比亚迪汽车产业群(比亚迪目前共有

IT、汽车、新能源和家电4个产业群)又在规划下一轮裁员计划,汽车产业群从现有的17000人调整至10000人,裁员目标数量高达7000人。

羊城晚报记者就此事向比亚迪相关负责人求证,但该负责人表示“未听到此消息”。但记者了解到,比亚迪“瘦身”计划近期一直在进行中。

比亚迪于2011年9月16日发布的内部通知显示,此轮涉及人员及组织架构调整的有比亚迪汽车工程研究院等8个部门。而将被直接撤销的部门则有汽车产业群总工程师办公室、第十二事业部和第十八事业部。

羊城晚报记者就此事向比亚迪相关负责人求证,但该负责人表示“未听到这个消息”。

这已不是比亚迪第一次传出裁员消息,此前8月底有消息称,比亚迪汽车销售公司将裁员近七成,但比亚迪方面对本报记者的回应称只是正常的“人事调整”,并未透露具体调整范围。

上周,比亚迪汽车销售公司一位高层领导在一个非正式场合向羊城晚报记者透露,近期比亚迪一直在“瘦身”。

上述高层坦言,比亚迪的“瘦身”错过了最佳时机。

2009年和2010年比亚迪有资金、有实力进行‘瘦身’,但是当时却急于扩大规模。据了解,2009年和2010年比亚迪在深圳、长沙等地都有新建或扩建项目,2010年比亚迪西安一个扩建项目还因违法占地还被国土资源部点名批评。

今年“瘦身”调整,又给比亚迪带来不少“风波”。知名汽车评论家贾新光撰文指出,不调整,比亚迪将真的会滑入无底深渊。

2011年9月26日 星期一

中國汽車增速 難以承受的快 朱鎔基轟不符國情 警告泡沫爆破

|

||||||

| 最新出版的《朱鎔基講話實錄》,最後一篇是「大力發展公共交通」。朱鎔基在講話中力批「小汽車狂熱」,認為不符中國國情。然而,在過去10年,中國汽車產銷量每年以25%的速度增長,於2010年已超越美國躍居世界首位。 汽車的超前發展,已為業界及社會帶來不少後遺症。專家分析,業界將面對產能過剩的問題;城市基礎建設跟不上,污染、能源消耗等也令不少城市無法承受。 污染塞車 生活質量降 無論從哪個角度看,過去10年中國汽車業的發展就像火山爆發一樣,速度之快舉世震驚。簡單地看一個數字,2000年中國汽車產量只有207萬輛,到 2010年國內汽車總產量達到1,826.47萬輛,超過美日成為全球第一。各大汽車公司仍摩拳擦掌,準備在「十二五」期間再加碼拓展,估計在2015 年,中國汽車產銷量起碼超過2,500萬輛。 然而,一些專家提出警告,在金融海嘯後,中國汽車業仍有高速增長,這主要是因政府連續兩年實施汽車消費刺激政策,引發大量消費者提前購車,從而出現透支消費局面。業界估計,在政策退出後,市場隨即會出現驟然降溫的情況。 實際上,中國汽車市場或許正在形成一個可能令國內汽車企業損失慘重的產能泡沫。一些分析人士擔心,由於中央和地方政府均在推動汽車業擴張,擴大後的產能 勢將超過需求。應當看到,目前消費能力最為強勁的一綫城市已基本處於飽和狀態,中國汽車只好向二、三線城市轉移。但一些主管汽車工業的官員認為,2010 年中國汽車千人擁有量58輛,不到世界平均水平的一半,不到發達國家的十分之一,足證中國汽車市場還有很大空間。 可是,實際情況是「汽 車災難」已為不 少城市帶來嚴重的社會問題,其中包括環境質量的嚴重污染、城市交通的嚴重堵塞,以及生活質量的嚴重下降。國家統計局總經濟師姚景源認為,中國汽車工業是神 話般的發展,但問題也接踵而來,比如說交通擁堵,現在堵車已堵到縣城;空氣污染,現在大城市空氣污染是因汽車廢氣排放太多。看到能耗、看到停車難、看到一 系列問題,各個地方都採取了一些措施,對汽車業的高速增長將帶來一定影響。 配合基建 拓公共交通 中國汽車技術研究中心主任趙航認為,中國路網建設、總道路面積不夠,路網建設也不合理,實際上損害了消費者的權益。道路建設和交通管理已滯後於汽車和交通發展,城市規劃、設計、安全設施缺乏遷延性和預見性。很多城市是按自行車或公交車出行的方式設計的。 此外,環境污染問題也令人擔憂。國家環境保護部污染防治司處長逯世澤指,據預測,「十二五」時期,中國還將新增機動車將近1億輛,這意味着將新增各種燃 油1億到1.5億噸,由此帶來的環境壓力可想而知。工信部一名領導更認為,2020年或2030年中國汽車有可能達到3億輛,按照目前這個排放的控制水 平,城市肯定無法承受,人群也承受不了,交通和燃油也供應不上。 「將來一垮 全部都垮」 工信部副部長蘇波最近在上海車展,對一眾車廠老總談到限車措施時表示,「世界上任何一個城市,即使公交、道路發展速度再快,也無法承受1年增加100萬輛汽車的速度。汽車消費要有停車場、佔用道路空間、排放污氣,政府對此不能不管。」 也許,政府及業界應回顧一下朱鎔基當年的文章,「不能一哄而起都去搞小汽車。小汽車一搞上去,需要一系列的原材料供應都搞上去,將來一垮下來又全部都垮。」「我們早就講過,中國不是這樣的國家,這個觀點我到現在都沒有變,應該以發展公共交通為主。」 | ||||||

2011年9月18日 星期日

不要做羊仔四個行業揀股

|

||||||

| 上星期五,一聽到貝南奇沒有

QE3,道指立即大跌至220 點;一聽到聯儲局延長下個月的會議,大家就憧憬QE3

會出台,道指即倒升百多點。這證明了全球很多人的投資素質都已變得好脆弱,不論發生甚麼事,只看到第一個人往左走,那怕左邊是一個火海,大家都會不經思索

地跟着跳! 與其做羊仔,跟着大家跳,倒不如想想哪些行業受全球經濟影響較輕微,以及兩三年內仍能保持超過二三成的增長,這樣做才更實際。 消費股跌後反彈力強 記得筆者於6 月中曾提出以下四個行業或主題,在未來兩三年內較少受到經濟大環境影響,而且增長明確,兼較少風險,所以建議圍繞他們來建立自己的股票組合:(1)高檔消費;(2)天燃氣;(3)保障性住房;和(4)澳門賭業 ■高檔消費 大家有否發現每逢大跌,所有股票大潛水後,最容易及最快回升上水面的是甚麼類型的股票?我認為是消費相關的股票。何解? 試想想recurring income 與on e-off income本質上的分別就明白。 上星期亨得利(3389)及英皇鐘錶(887)公布的中期業績都遠超市場預期的上限,但是公布後翌日,股價的表現都非常相似,早上上升4%至7%,然後收市倒跌,何解? 還 記得今年第1 季時,零售股被不斷沽售,券商de-rate 完再de-rate 後,大家還覺得股價不吸引的情況嗎?當時六福(590) 由28 元下跌至19元,跌幅超過三成; I.T(999)由7.7 元跌至4.5 元,跌幅更驚人,四成!我不敢說當時的環球氣氛與現在一樣,但可以肯定的是我不見得他們的基本因素有很大變化,特別是高檔消費股。 亨得利和英皇鐘錶好於預期的業績,也是對六福及東方表行(398)的一個很好的啟示,相信他們4 至7月的業務也不會差! 筆者喜歡參考未來12 個月的市盈率,而不是2011 年的預測市盈率,因為大家會隨着時間不斷估算下一年的情況。以下是珠寶鐘表股未來12 個月預測市盈率:六福─16.4 倍;亨得利─15.5 倍;英皇鐘錶─14.1 倍;東方表行─8.9 倍。 吸不吸引,自行判斷吧! ■天燃氣 筆者一直預期天燃氣分銷將會於2015 年前處於穩定的快速增長期,一般來說, organic growth 20%加上收購合併的10%增長,每年的增長率應在30%或以上。 看看各燃氣股的中期業績,港華燃氣(1083)盈利增長7 成以上,華潤燃氣(1193)增長接近7 成,新奧燃氣(2688)增長35%,筆者實在不見得外圍對他們的業務有何大影響。 ■保障性住房 不 用多說,在筆者眼中,保障性住房的不二之選是中國建築(3311)。8 月從高位8 元下跌超過26%,至昨天的5.87 元,近來不斷有人認為現在市盈率很高,很貴。何謂貴何謂平?升市時大家覺得它10元也很平,跌市時5 元也會說貴,當大家在羊群時,平與貴很多時就是隨波逐流的直覺判斷。 另外,有說五年目標建3600 萬套的計劃會減少,筆者不信,我認為最多調整每年的開工目標,而不是五年總目標。有人說由於限購令導致地產發展商被迫湧至發展保障房,把利潤率拖得更低, 筆者認為有可能,但不會影響中國建築,因為大家的模式根本不一樣! ■澳門賭業筆者不是賭仔,不懂賭仔的心態,是愈窮愈要賭?還是中國人的愛賭特質是唔理三七廿一,總之要賭? 由2010 年至現在,看看每月的澳門博彩收入公布的數字,幾乎每次都創新高,實在不知道何時才是結束的高增長的時候,筆者樂意看到8 月或9月的數字顯示較慢的增長,然後成群羊仔沽售濠賭股。 | ||||||

豪華汽車品牌攻城略地

豪華汽車品牌攻城略地

比起自主品牌及30萬元以下合資品牌車型的促銷和降價策略,豪華汽車品牌的江西經銷商在9月份的策略,卻依舊是攻城略地,絲毫不給市場以喘息機會。

9月9日,上饒寶澤4S店在月亮灣汽車城正式開業。這是華晨寶馬繼南昌、贛州之後開設的第四家授權經銷商。“說實話,寶馬汽車現在的訂單就已經要排隊到好幾個月之後去了。也就是說,因為供不應求,有些車型即便現在訂車,估計年內都很難提到現車”。採訪中,上饒寶澤4S店總經理劉躍輝表示。

對於9月攻勢,奧迪汽車經銷商也表示,豪華品牌跑馬圈地一方面說明其銷售和網絡渠道下沉至二三線城市,欲促進和分享江西地方經濟發展的成果,同時也說明瞭車企產能擴張的預期。“8月份的銷量回升,讓很多人大吃一驚,同時也印證了金九銀十的市場規律”。

期盼車展更多促銷政策

“今

年上半年車市一直很低迷,尤其是前幾個月,大家以為汽車價格還會降一降,沒想到8月份市場就開始回升了。據說10月1日之後很多汽車的節能補貼政策都將調

整,市場上可供選擇的車型也會少很多。”在東風日產南昌4S店,前來看車的市民王駿表示,原本打算年底買車,但看到現在這樣的市場行情,又忍不住想出手

了。

無獨有偶,記者在採訪中發現,有王駿這種糾結心理的潛在消費者不在少數。大家一方面看到了現在汽車消費的利好政策,一方面又覺得七城運會前南昌交通狀況極大的改善,行車方便的優勢,在這種雙重影響下,對買車不免有些心癢。

“對

汽車廠家來說,南昌、九江、贛州二三線乃至三四線城市,越來越被看重,加上南昌國際車展日益臨近,消費者對汽車的關注度也越來越高”。業內人士表示,對於

具體車型的促銷政策,如需急著用車的消費者覺得價位和服務在承受的範圍之內,可以出手提前預定。不過,10月份屬於第四季度,對很多經銷商來說,真正的營

銷殺手鐧可能還是會放在車展上。

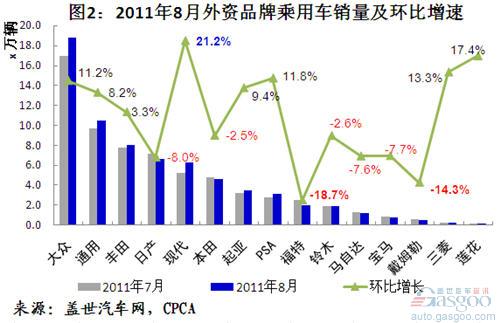

2011年8月外资品牌乘用车销量变化

2011年8月外资品牌乘用车销量变化

据盖世汽车网整理的乘联会批发销量数据,2011年

8月,15家外资车企在华国产外资品牌乘用车在华销量(本文指轿车、SUV、MPV销量之和,以下简称为销量)68.46万辆,同比增长14.5%,环比

增长5.0%。这些外资车企按国产车销量高低排名依次是:大众、通用、丰田、日产、现代、本田、起亚、PSA、福特、铃木、马自达、宝马、戴姆勒、三菱和

莲花。其中,销量超过十万辆的有大众和通用,今年8月份销量分别为18.82万辆和10.48万辆。

与去年同期相比,此排名主要变化是:现代被丰田、日产超越,排名降至第五;起亚超过PSA,排名升至第七。与今年7月相比,此排名保持一致。

同比:莲花和起亚增长最快 马自达降幅最高

从今年8月销量同比增长率来看,这些外资品牌中销量增长最快的是莲花和起亚,两家企业分别增长46.1%和40.0%至1756辆和3.50万辆。

其中,起亚老车型均销量均出现下滑,其销量拥有较高增速主要靠新车K5、K2和智跑(分别于今年3月、7月和去年10月份正式上市)所拉动。

除莲花和起亚之外,丰田、日产和宝马也均有30%以上的增长,增幅分别为37.4%、30.7%和36.5%;大众、通用和PSA销量分别同比增长10.3%、26.1%和22.7%。

现代和戴姆勒销量均以个位数增长,分别增长3.6%和2.1%。

而销量出现下滑的外资品牌有日系本田、铃木、马自达、三菱和美系的福特。其中,马自达下滑幅度最高,为29.3%;其他三家日系车企降幅分别为3.6%、9.2%和9.4%;福特同比下滑7.2%至2.03万辆。

环比:现代增长最快 福特和戴姆勒降幅最高

从8月销量环比增长率来看,15家外资品牌中,环比出现正增长的有8家,分别是大众、通用、丰田、现代、起亚、PSA、三菱和莲花。其中,现代环比

增速最高,达21.2%。其次是莲花、三菱、PSA和大众,销量也均以两位数环比增长。而通用、丰田和起亚销量均以个位数环比增长。

销量环比出现下滑的外资品牌有7家,分别是日产、本田、福特、铃木、马自达、宝马和戴姆勒。其中,福特和戴姆勒环比降幅最高,分别为18.7%和14.3%。而日产、本田、铃木、马自达和宝马销量均以个位数环比下滑。

注:

宝马7月中国市场销量骤增36.1%

宝马7月中国市场销量骤增36.1%

盖世汽车讯 据路透社报道,宝马日前公布了7月份在全球及各主要国家市场的销量数据,全球范围内销量同比增长7.6%,而中国市场的增幅水平更是达到36.1%。中美两大主要市场的提振成为宝马7月销量上行的支柱。

宝马官方表示,7月份宝马、MINI及劳斯莱斯各品牌总销量为129,094辆,较去年同期的119,992辆提高7.6%。其中美国市场销量从去

年的19,064辆同比增长12.3%至21,409辆,交付量(Delivery)则从23,390辆增长11.7%至26,120辆;宝马再度成为美

国市场最畅销豪华车品牌;中国市场销量由去年的13,852辆同比增长36.1%至18,858辆;反而德国本土宝马新车注册量同比略下降0.8%,从

23,397辆减至23,212辆。

宝马销售总监Ian Robertson表示,该月达到历来最高的7月销售数字,正在向着2011年总销量突破160万辆的目标迈进,创下宝马集团史上的最佳年销售业绩。

2011年宝马一直保持了较高的销量增幅。今年前7个月份,宝马总销量较去年同期的816,014辆增长17.9%至962,468辆。

迟来的消息,但对华晨汽车1114应该有正面的推动.

宝马高管称公司今年8月全球销量突破10万辆

盖世汽车讯 据路透社消息,宝马高管称公司今年8月全球销量突破10万辆,推动2011年完成160万辆销量的目标,同时将宝马利润率维持在较高水平。

日前宝马CFO Friedrich Eichiner在接受《法兰克福周日新闻》记者采访时表示,今年8月份宝马汽车的销量突破10万辆大关,同比增长约为7%;在美国和欧洲市场的销售业绩均达到两位数的增幅。这表明宝马受到全球经济衰退的影响甚微。

Friedrich Eichiner表示,8月份的成绩有利于推动宝马原定2011年销量160万辆的目标,同时将达到10%以上的销售利润率,预计到2012年之后仍将保持8-10%的毛利率。当前宝马的订单形势较为乐观,未来数月开工率可保证订单顺利完成。

上周四,宝马宣称在美国市场前8个月总销量同比增长幅度为14.6%。

Value Investing - Making it successful in China

Thank you very much, Professor.

Professor Bruce Greenwald, I appreciate the opportunity to speak today. I want to say thank you again to the Heilbrunn Center for Graham & Dodd Investing and Columbia Business School, and of course I am deeply grateful to all of you for coming. I will try my best to share with you what I know about how to apply the value investing discipline in my part of the world, East and Southeast Asia.

Now, before I go on, I need to tell you, according to Compliance regulations, that the statements that I am about to make to you represent my personal opinions and not those of Value Partners.

As for Value Partners, we are the only listed asset management company in Asia, outside Japan, and even in Japan there is only one listed company, so there is ample documentation available on who we are and what we do; there is a lot of transparency.

The company was listed in 2007 by Morgan Stanley and JP Morgan. The mission of the company is very straightforward. Our mission is to build a temple of value investing for East and Southeast Asia. This phrase was coined by yours truly. Actually, I used to be a journalist; I worked for The Wall Street Journal in the 1980s. But seriously, what we are really trying to say with this phrase is that we are first and foremost a value investor, and only secondly are we a China investor. The distinction is quite important, because up to now, China has been what I call a ‘story’ market. A lot of people buy and sell China based on stories they read in the press or on what somebody has told them about. In the process, it can be very difficult to carry out fundamental value investing according to the textbook definition.

So, we are trying to go the other way. Our standard textbook throughout the 1990s was Graham & Dodd’s Security Analysis. We actually applied it quite religiously; we used to call it the Bible. But in more recent years we switched to a different book. I am not plugging the book, just telling you what we do. It is a book by a guy named Martin Fridson, whom I never met, called Financial Statement Analysis. It is a simpler book, but pretty much the same thing as Security Analysis.

We’ve conducted about 2500 company visits per year, excluding phone calls. That is the real source of our power; just old fashioned kicking the tires.

So, we do a lot of financial modeling. We’ve conducted about 2500 company visits per year, excluding phone calls. That is the real source of our power; just old fashioned kicking the tires. What we are good at is that we put into practice the theory of value investing that my colleagues and I have read about and we’ve study very seriously.

I actually do not believe we have anything original to say about the theory, but I think we have gained some valuable insights that I will share with you about its actual application; this is what we are actually good at. Now, before I go on to the next slide, I want to tell you that by the roughly mid-to-late 1990s, I was coming up against the big “what if” question, as I tried to create a sustainable business model out of the concept that I wanted to carry out value investing in this very immature market that we call China. Because I began to ask myself what if we can create a business model – a value investing firm – that performs, but that is not dependent on having a genius or a star performer or some kind of a magical black box within the firm?

I even began to wonder if there was some kind of a conspiracy, maybe by the marketing people or the press, to try to tell the story that to beat the market you needed to have a genius or a star performer or a black box, and I thought to myself that this was not a very sustainable way of doing the job. So, I began to ask myself very straightforward questions like, is there a way that normal people, ordinary people that you recruit out of college, can become very good value investors, at least with respect to the China region?

So, that became a kind of quest for me. Initially, it was just intellectual, but as I am going to explain to you over the next 15 minutes, we turned it into a reality.

First of all, you have got to understand that if you do not have good people you cannot create a good product. So, the first answer to the puzzle or the question I just raised is to create a very good corporate culture. And the second thing we do, which is, I think, a bit more interesting, although I know that sometimes when I say this, I am greeted with a bit of hostility from people who do not want to hear about this. I believe I have succeeded, to some extent anyway, in industrializing the value investing process, transforming it from a boutique craft into a process of mass manufacture. It sounds pretty elaborate, but actually is very simple.

Again, I will explain to you, but I am trying to get away from a system that relies on geniuses, and trying to get a system that I turned into a sustainable and a scalable process. In fact, we have been doing this in Hong Kong since the late 1990s – sometimes with great difficulty. Sometimes, we thought better to just give up, but we stuck to it and we have in the process created, what I think, is a pretty valuable business that in fact has consistently been able to beat the market.

I believe I have succeeded, to some extent anyway, in industrializing the value investing process, transforming it from a boutique craft into a process of mass manufacture. It sounds pretty elaborate, but actually is very simple.

of Merrill Lynch. That was the first mainland China company. Today, of course, it is the partner of BMW in China.

Things happened at Value Partners too quickly; there was not enough time to put together an in-depth and appropriate culture of professional integrity. That is why you sometimes hear some great horror stories. Very basic concepts that should have been instilled in the market when people first joined, concepts like put a client’s interests first, be transparent in your dealings, identify and be wary of potential conflicts of interest… You would be amazed by how many people in my industry, in my part of the world, have never heard about it or only pay lip service to it.

So the first thing I did was – actually not the first, but sometime in the mid-to-late 1990s – I pu t together what I call My Promise, and I asked my staff to sign it, individually. I framed it and put it in front of them, in front of their computer, so they would be reminded of it every day. And we do a lot of this brainwashing thing, you know, that we have elaborate ceremonies and kind of assure one another that we are very serious about our Promise.

So, here is a copy of the promise and it basically just encapsulates basic concepts that you need, because value investing is really a kind of a very vigorous philosophy and deep exploration of reality, but if you don’t have people who are intellectually even honest, there is no way you can carry out the mission.

The first part of what we do is that we had to start from almost ground zero in terms of creating an appropriate culture to implement and execute this concept. Here, I have to take two steps backwards and explain to you the context in which I operate, because here I am in a market that, unlike in the United States, is a very young and immature market. The first companies from Mainland China were only listed in 1991 or 1990, I cannot remember; there is a company called Brilliance China, and it was listed in New York with the help

mass manufacturing and industrializing a craft, what I really meant was that I have broken it down into a set of skills. Each skill can be mastered by fairly ordinary people with probably just a college education, and the process is teachable, is repeatable, is sustainable, and is scalable. It is definitely not magic, it is definitely not driven by genius, but it is all the above that I mentioned to you.

I would identify each of these skills to you, but the starting point for this is that there are a number of images I can draw for you to try to communicate what I am actually trying to achieve.

One is, I was very frustrated by the idea that no matter how smart a human being is – even the President of the US, for example, who is after all just a human being – his potential for excellence i s almost defined by the limitations of being human. But what I really want, if possible, is an operation or situation that can be almost beyond human – superhuman – and then I thought of the concept of the ant colony.

There is a saying that in case of an all-out nuclear war, the human beings won’t survive but the ants will. Why is that? Each ant is probably a pretty dumb animal or insect, but together, by socializing the process involved in survival and production, they are incredibly strong. You can’t really kill them all, they are repeatable, they are scalable, etcetera.

Each human being has different strengths and weaknesses, but together we make a formidable team.

Finally, I thought about what Chairman Mao said, or was alleged to have said. I was too young actually, but there was something about using socialism to help capitalism. So, as a company, we are a pretty socialist company. I won’t go into big detail, but people have compared us to being Israelis on a Kibbutz – everyone helps each other, but we are actually doing all this in cause of the capitalist system actually.

Anyway, so what we are really doing is that we have broken down each skill into steps and here are the steps, these are the so-called seven specialist skills.

The first skill, obviously, is originating ideas. Original ideas itself is an important skill. We have a matrix, let us call each of it A, B, C, D. I’m quite proud to tell you that I actually scored A in originating ideas, but unfortunately, in some other skills I have like a C.

Each human being has different strengths and weaknesses, but together we make a formidable team, I think. So, for originating ideas for a value investor in China and Hong Kong, the key is to find ideas that are very contrarian. Perhaps I should illustrate it on the board. I will go through each skill step by step and tell you or highlight the salient points that we use to train people for each skill.

For originating ideas skills, which I claim to score an A, we have a universe of several thousand stocks: Taiwan, Mainland China, Hong Kong, and in the case of Value Partners, some Korea, Japan and Southeast Asia. We simply divide all the stocks into category 1, 2 and 3.

One is undervalued, so your job if you work for me or in my team is that you must try to identify Category 1 stocks and then do research on it. Category 1 stocks are undervalued. Category 2 is fair value. We find a lot of sell-side brokers tend to recommend Category 2 stocks.

And, when you sit in a taxi and the taxi driver tells you about stocks, it is probably Category 3.

So, technically, our objective is to buy 1 and sell at Category 2.5. Later I will start telling about the problems, but anyway, right now I am just giving you the theory. For Category 1, generally, the most fertile area to find these ideas are stocks that are unpopular that nobody cares about – definitely not an index stock, or that something bad has happened. It sounds so simple, but in real life it is quite difficult to do because maybe it is Asian culture or human nature, but people do not feel safe sticking their necks out to look at these unpopular companies.

So, in China-related stock markets, there are actually quite a lot of Category 1 stocks because it is a very emotional market, very momentum driven, so stocks fall in and they fall out of favor fairly quickly, and, in fact, in a rather predictable way. Now, in case you can identify good Category 1 stocks, your next step is to start looking at the research part of it. Remember, I said this was skill number 2.

Research, now for a firm like Value Partners, and I think a number of firms around the world, is

quite difficult to push out to the frontier intellectually. We have standardized our spreadsheet, and we look at all the obvious details and financial numbers and number crunching. The only thing new I can say about research is that in the China context, we have been moving increasingly away from quantitative analysis to qualitative analysis. When I first started in the 1990s, there were very few companies with superior business characteristics in China. What you were really buying were pretty lousy companies trading at very cheap prices, and that, in fact, it was quite difficult to be a long-term investor because some of these companies got chopped up, or competitors came in and they are gone.

So, we were pretty much a traditional classic value investors trying to get the last free puff of the cigarette. But in more recent years, the trend has been much more encouraging. You are finding more companies that may fit the description of a good franchise. I.e. a sustainable, competitive advantage, durable advantage we call it, and to do that it is very difficult to quantify in numbers.

So, in China-related stock markets, there are actually quite a lot of Category 1 stocks because it is a very emotional market, very momentum driven, so stocks fall in and they fall out of favor fairly quickly.

You have to look at the characteristics of the management and the business model. But in summary, we are looking for something called the three R’s: the Right Business, run by the Right People at the Right Price. And as I mentioned earlier, we are seeing a trend where the original emphasis of Value Partners on just the Right Price, because it was the only thing we haven’t found, is changing more and more to the Right Business run by the Right People.

The third skill was originally not considered a skill until I began to realize that decision making is in fact a teachable skill in itself. Actually, the real problem is the lack of decision making, because although we had a team of almost 30

people who were analysts and fund managers, few people actually wanted to stick their neck out and make a real decision.

We call that a lack of killer instinct – this is one of my phrases. Nobody really wants to kill anybody anymore in our civilized world, you know. So, we even have a guy who has since left the company, we called Mr. OTOH.

OTOH stands for ‘On The Other Hand’.

Yeah, I’m sure all of us know about this, that the analyst will always give analysis in about 30 pages that take you half the night to read, and the conclusion is: however, if, but, and on the other hand, you know. So, in the end, you don’t know what you are supposed to do, if anything.

So, I am trying to kill the Mr. OTOHs in my company, but it is not easy, and I began to realize that it is possible to train and be good in decision-making. One clue to the way we are doing it is borrowed from the Buddhist philosophy, which I am a follower. It is to remove yourself, your sense of self from the equation, when you are trying to analyze anything. By injecting yourself or your sense of ‘me’ into an analysis, you distort the reality because your ego gets involved. Your perceived self-interest, your need to be given credit for something, gets involved. So, remove yourself from the analysis.

Now, the next cue, we call it “deal structuring.” This again came about almost by accident, because I began to realize that by local Hong Kong standards, we are a very big company.

But anyway, we are a big guy in our little patch of the jungle, and we can demand good treatment from the brokers, and I began to realize that if we decide to buy something based on the research and our idea finding, we shouldn’t just go and try to buy in the stock market. We should approach the company and say, let’s make a deal: we’ll buy 5% in your company, and you do it through a form of placement of a single block of shares or what the American people call “PIPES” transactions, which I think stands for privately something, something per equity, whatever, you know.

You always get better terms, more discount, or you can get them as convertible bonds. For your information, about slightly over a year ago, an American company called Affiliated Managers Group, listed in New York City – the chairman is over there. They bought 5% of my company through a negotiated deal.

All right, so due structuring in itself just brings a lot of benefits to clients.

Now, the next skill I think we’ll mention is Execution. This is no longer done by our fund management team. It is actually done by a specialized team of full-time dealers; we have three of them in the office. It is in itself a specialized task.

Then, from here on my scores are dropping, for your information. I tend to get high scores here and lower scores as we go along because I get bored as we go down the sausage-making machine.

Maintenance – this is just a fancy word for saying, “after you buy the stock, don’t forget about it.” Keep in touch with the company, update your research vigorously, and keep thinking how you can continue to enhance the value of the investment.

And the final thing is Exit. For people like me, Maintenance and Exits are weak points, and I tend to try to delegate it to other members of my team who are more interested in these particular skills. Exit means actually selling the stocks, and the prevailing wisdom for this is that you are supposed to exit when you figure that what you know about the company and the people in the company is quite common knowledge to everybody, so you have no more value to add to the investing process.

Then you should be getting out; in theory. In real life, we usually sell far too early. I think it is a thing about value investors. We see a lot of problems all the time.

I think it is a thing about value investors. We see a lot of problems all the time.

All right, sorry, just a short intermission. In case you are the CIO, you have to master these additional skills that I had not mentioned earlier. The additional skills are: providing leadership, to make things happen – macro strategy – which we didn’t use to think about as a skill, because we were diehard, bottom-up value investors, until the Asian financial crisis. And then we realized that you actually better have some idea of what is the overall macro environment you are operating in; asset allocation and portfolio construction. This is not done at the fund’s managerial level; it is done at my level.

I am actually the Co-CIO with another guy named Mr. Louis So. We two guys are responsible for these skills, for better or for worse. We try to provide leadership to the team, motivating people. Here, the key take-away you should note is that there is an abundance of hard skills in Asia, but a shortage of soft skills. What do I mean by that? For your typical Asian people, if you can sit an examination and provide some text books, they would do very well; they have that kind of culture. But if you ask them to do things that are not so tangible like communicating with people, motivating people, providing leadership and leading, they are not so good. I am not sure why that is so, but it is a fact. So, we tend to struggle a little bit in finding people who are willing to be leaders or to even communicate properly with people in the office leadership.

Macro strategy, I am not a macro expert, but because of my perhaps size and experience, I am plugged to people who are macro experts, and I make sure they give me the first call if they think anything is worth talking about. That is probably good enough, but you have to have some sense of the environment where you are trying to put money to work, although we remain primarily a bottom-up stock picking company, and asset allocation and portfolio construction must take into account your evaluation of the macro environment.

So, more or less as an example, we went from 10% cash in our funds to 1% cash in our funds between June and July this year, because, from a macro point of view, we concluded this is one of those windows that opened up for China investing where you should be very aggressive when putting money to work.

The right way to go to do our job is that if you enter a transaction if you are a buyer, you shouldn’t be buying if you think the seller knows more than you.

Negative interest rates, soft landing, now increasingly evident for the China economy, and

various other factors, including inflation, are likely to increase a harder landing because the Hong Kong dollar and the US dollar are pegged, so we are importing a lot of loose money policies from the US, even though our own economy is actually doing very well. So, the adjustment is taking place through asset prices.

I want to share with you at this point, the halfway mark of my prepared remarks, that internally we no longer call ourselves ‘value investors’, although of course we are, you know, otherwise I don’t think I will be invited to speak to you today. But internally, we use another phrase now. I won’t write it because it’s easy to remember.

We call ourselves ‘advantage investors’, which is part and parcel of the seven skills approach I mentioned to you.

I have developed and written quite a number of memos internally on the concept that the right way to go to do our job is that if you enter a transaction if you are a buyer, you shouldn’t be buying if you think the seller knows more than you.

If you are a seller, you shouldn’t be selling if you have not clarified why the buyers are willing to buy from you. This is a simple advantage idea; that you must always have some confidence that you have an advantage over the counter party in any transaction, and we have developed many theories about advantage, most of it is based on the idea of having more research.

Here we are blessed, because unlike a relatively more efficient market like the US, our markets are extremely inefficient. We have all sorts of people who are not qualified to be in the stock market but who insist on being in it anyway. I had many experiences where I asked people, “what is the purpose of the stock market my dear?” And they are, “Oh! It’s there for you to make money.”

That is all they will say. They forget that the market is there to mobilize surplus savings of a society and put it to work in productive enterprises. Nobody cares about that actually; asset-wise, maybe.

But anyway, so if you take the trouble to research and do company visits, you have actually a pretty strong advantage over many other players in China-related stock markets who are actually quite, you will say, ‘uneducated’ in the true sense of the word.

You definitely can practice advantage investing. Portfolio construction at my level is mostly based on the idea of taking advantage of the macro environment and highlighting your core competence. Actually, we only have one real core competence: stock picking.

So, the portfolios that I run are all designed to – as Professor Greenwald mentioned earlier – to gather against the downside risks, while participating in the upside through a construction system that basically allows us to shine in the one thing we know best: picking stocks.

This process allowed us to grow our fund size in a way that couldn’t be done if our business model was based on a single human being, a certified genius running the fund.

I am going to go on because it is time to talk about overall things I learned about how to survive and prosper in China-related markets. Here, I am leaving one of my main subjects, which is how I think we are trying to industrialize the process of investing, but before I go away from the subject, I want to emphasize again that when I tried to describe this process to some clients, I noticed that they were not very happy, because they thought this is a some sort of a trick for us to become an asset gatherer, that the reason we have this industrialized process was because we want to get big.

This process allowed us to grow our fund size in a way that couldn’t be done if our business model was based on a single human being, a certified genius running the fund. But here we can have many, many people are doing it, right?

But I just want to assure you this is really not true. The truth is, from the 1990s onwards, I was very interested in knowing how we can develop a sustainable business model for running money, and yet beat the market consistently, and yet depend on hiring normal people to join our company. Not great people, but just normal people who can, however, become great, and also a system that we help each other with our weaknesses, in a very humble and frank manner.

Okay, let us talk about Asia as a whole. First of all, I already mentioned it is basically a very

inefficient market. You don’t necessarily make money by investing in superior businesses. As I said, there is a growing number of such superior businesses, but it is still much less than in America. You make money by taking money from stupid people who shouldn’t be in the market; that is the truth about it – it’s changing but it’s stil l there.

You need to be familiar with the political and social context of the investment, not just the financials. We have problems sometimes with Asian people who came out of US Universities with an MBA or whatever, because we find that they are too focused on numbers alone. Actually, there is enormous baggage in Asia regarding its history. Some people are very sensitive about politics and social issues. You have to be sympathetic to it. You have to understand why sometimes so-called irrational things are done. I think even the Chinese Government, from my feedback now, is beginning to realize that growth for the sake of growth is not that ideal.

There are a lot of other things that are important, like having a clean environment, reducing the income gap between the rich and poor, countryside and cities, and not just growth for the sake of growth, and this is in the same context that you must understand what makes people do what they do. Because of their history, their social values, etc.

One exercise we try to do sometimes with some success is, we imagine what the newspaper will say about the company we are investing in, six months from today, 12 months from today, 36 months from today.

I think it is probably because of my own background as a newspaperman. It is very useful when you look that way; that you can imagine, close your eyes and imagine, because you will find that sometimes the outcome for your particular company, whether it is a car company or an agricultural company, is driven not just by numbers, but by government policies and sometimes even by, let us say, the phenomenon called El Nino, which is a kind of a temperature, climate thing that is sweeping the Pacific right now.

Now, the last one I will say again is something that I noticed. Sometimes, people don’t want to hear from me but I have got a secret that I will share with you. When I first started my job with Value Partners in 1993, I was like every other US-

trained or US-inference fund manager. I believed in having a very concentrated portfolio. I used to go around telling everybody “you won’t see more than 40 companies in my fund, these are my high conviction ideas,” and I was very proud of it; and then as the years went by, I began to realize that our market was really very different from the US, because there are just a lot of crooks out there with very bad corporate governance, and some of these guys are very convincing.

I used to go around telling everybody “you won’t see more than 40 companies in my fund, these are my high conviction ideas,” and I was very proud of it.

So, your high conviction idea may turn out to be actually your next lament, you know. But you won’t know until you wake up the next morning and read about it in the newspaper that your investment, which makes up 5% of your concentrated fund, has just evaporated overnight.

It happened to me quite a number of times, so I have many scars with me. So, in the last, especially 10 years, I’ve swung to a different view. For emerging markets such as China, it is better to have a very diversified portfolio. Don’t put more than say 1 to 2% of your fund in any particular idea, because you can then go to sleep much better and you can withstand all these nasty accidents that seem to happen every now and then, no matter how hard you work at it.

So, now we have a portfolio with typically over 80 to 110 companies inside. Now, why don’t more fund managers do what I say; it’s because there is a lot of self-interest. Few fund managers don’t have the kind of research resources that I do . If you have a research team of maybe 5 people, it is already quite a feat to have a fund with maybe 40 ideas inside; but we have the resources. We have 100 companies and we still have the resources to come up with 100 top-notch ideas; and that is what we are doing. Keep it diversified, be able to withstand the unexpected bad guy who smiles at you, shakes hands with you, and then disappears with all your money very suddenly, you know.

As professor Greenwald was saying, it got the downside risks, you see, not the variation. Keep it diversified.

Now, the next phenomenon I want to tell you about is that our industry over there is surrounded by pirates; not Somali pirates. By this, I mean stock promoters whose full-time specialty is giving you very convincing presentations and getting you to put money into their projects or companies. I am very familiar with this phenomenon. I have lost some money to these guys, too.

It partly has to do with what I mentioned earlier, the fact that it is a young market and it takes time for the proper values and professional integrity to develop. So, you have all these well-dressed young men and women who specialize in talking to fund managers like me. They know that we control a lot of money, and unlike banks we do not really have credit evaluation, we just decide. Sometimes, within the same day, we can give you tens of millions of dollars of other people’s money to finance your project if your presentation sounds right.

So these days, if someone comes to see me who has got the right university degrees and attire and speaks like my kind of language and tells what I want to hear, I am actually very suspicious. I’m not relaxed at all. I now have a history of preferring people who are pretty rough and ready, and look like they just came out of the shop floor. That is my kind of person now.

I mentioned earlier about abundant hard skills, not much soft skills, and here is the other thing about our industry. Because of the incredible growth and abundance of wealth created so suddenly in just 20 years by the financial industry in East and Southeast Asia, everybody wants to join in. Even people who are not the least bit interested in finance. This is very unhealthy. It has created a phenomenon that I call the money disease, where people join because they think they will make a lot of money not because they are interested in our profession.

At Value Partners, we usually have an induction class that within the first 3 months, I will personally give you a talk where I try to explain to you that your name is your brand. If your name is John Smith, then John Smith is your brand. It stands for how people will see you in the years and the decades to come, and you can very

easily spoil it by becoming a victim of the money disease, putting money in front of everything else, whereas money in fact should be a byproduct of professional excellence.

If you are very good in what you do, money will find you, you don’t have to find money. It reminds me of Sash Spencer.

Okay, I jumped the slide a little bit. So, your name is your brand. Now, the next thing we want to do is that we think that the disease of fund management is ego. People who have had some success being money managers, they are very vulnerable to the ego disease. They think they are God and we try to discourage that. For example, we have this Master Big Theory of how you see yourself. If you see yourself as smart, you are likely to do stupid things. If you see yourself as stupid, you are likely to do smart things.

You can very easily spoil [your personal brand] by becoming a victim of the money disease, putting money in front of everything else, whereas money in fact should be a byproduct of professional excellence.

So, we try to tell each other, let us see each other as stupid people. It is better to assume we are stupid. And we also find, at least for our team, people tend to overreact to almost everything. It is that kind of office: we are nervous, we are jumpy, there is a very high energy level. The average age in my office is about 30 to 35 years old, lots of surplus energy.

So, I had to train people before you even decide what to do, decide how much you are willing to invest emotionally, and as a reaction, to any situation. Once you have decided it should be no reaction, some reaction or a lot of reaction, then decide the contents of your reaction; what exactly and how you want to react. And of course, be a contrarian, as always.

I want to show you how all these years of fighting and being hurt and trying to be the best is possible. My own signature is “Learn.” I changed my signature when I was about 25 years old from my name to “Learn,” so that I can remind myself every day when I sign my name to be humble and

learn new things, because I think the commitment of learning is one of the major characteristics of a civilized and responsible human being, whether you are a fund manager or you are not a fund manager. But if you are a fund manager, even more so.

So, timing is good. I’m on track.

I just want to end the formal presentations and invite your questions by summarizing some slogans you will see on the walls at Value Partners, my office in Hong Kong.

We try to be small enough to be effective, big enough to be strong.

This is probably the subject of another speech, but essentially, even though we have grown to up to 100 people, I have been trying the various concepts and theories to divide the theme into small boutiques, so that each person working in Value Partners would not have a big company disease.

He or she is actually working for a small group of only 5 people, and they have to think like a boutique and perform like a boutique. I am still facing some difficulties in executing this concept… That’s for the next speech.

Also, I think I told this earlier that we try to create a company where we depend on ordinary people and try to turn them into extraordinary performers.

Because I think it is not sustainable for a business model to depend on the constant inflow of geniuses to join you, and even if they do, they may not stay for very long.

Finally, I started these formal remarks or discussion by saying that I don’t have much to say about theory, but we have gained a lot of insights into the practice of value investing. In fact, I would end by saying that how you see yourself is very important, and very often I find that I am my own worst enemy.

My own error rate is about one third – about one third of everything I do. With hindsight, I wish I had not done it, but it is done, it is too late. So, the way I see myself and the way my young people who are working with me see themselves is that we think of ourselves first and foremost as soldiers. You know, we don’t wear a uniform, we don’t carry a gun, but we act very much like real soldiers, very disciplined, very committed.

We don’t have any breaks, and we know that we are engaged in a war that never stops, the war for performance, and these things are not very theoretical for us because we actually mean what we say.

Thank you so much.

Professor Bruce Greenwald:

All right, we’ll go ahead and take questions. Can we turn the lights up a little so we can see the audience? I mean, I would be happy to take questions from the audience if there are ones out there, since – Ah. Yes.

Speaker #1:

Thank you very much. Thank you for your kind remarks. Two questions really. You mentioned that you are finally finding a fair amount of quality companies with enduring franchises in Asia. Right? Quality enduring franchises. Two-part question. When we look at the non-SOEs in China, the non-SOEs, how many do you think will be allowed flourish over a number of years? I mean, I see they are confiscating BYD’s land; there was an article in Bloomberg last week about a private auto company being forced to merge with an SOE for political reasons – that is part 1. Maybe an easier question is, since about 90% of the SOEs’ CEOs are appointed by the communist party, what is their principal objective? Is it really to maximize shareholder value or to promote the communist party’s agenda regarding China?

Mr. Cheah Cheng Hye:

Actually this is a fundamentally credible question, because the economic and political system of the People’s Republic of China is not capitalism in the American sense. It is a form of authoritarian state capitalism. So, your question reflects the reality of what this actually means. The SOEs are there to carry out the concept that the party remains in control, although at the working level we have a system of material incentives and backup forces to promote an efficient economy. Now, having said that, I am not allowed to show you for compliance reasons my performance, but I can tell you verbally without giving you numbers because of the restrictions, that we have flourished essentially by focusing on private chips.

Private chips is the jargon used by the industry to describe non-state enterprises. From the 1990s onwards, I figured that these big gigantic state-owned enterprises were not my cup of tea. So, I went on my way to cultivate a small number of

private entrepreneurs who were allowed to flourish, and we took big stakes in them. Some of them let me down; they are some of my worst losses, but those that you make money. You make 10 beggars, you make 20 beggars, and they are still your friends till this day.

So, the whole Value Partners fund was in fact a kind of antimagnetic fund in the sense that the main game about China is the state-owned enterprises, but we went the other way. We focused on the small number non-state enterprises, and the answer to your question, by the way, is that forced mergers between private enterprises and state-owned enterprises, as far as I know, are not a major issue in China. It gets reported by the media like Bloomberg, partly because the Western media, of which I used to be a representative myself, is very ideological. They tend to pick on those stories and highlight it, but this is not the main landscape. This is only part of the landscape that interests a Western audience.

Rest assured that most private enterprises in China are left to their own devices for better or for worse, but the real body is not a level playing field. If you are the private enterprise you don’t get access to bank lending, bank loans; you don’t get access to privileged locations, and you have to wait a lot longer for licenses and other things. So, the playing field is very unfair if you are not a state-owned enterprise. And the way to get around that is to be corrupt – yes!

So, there is a saying that may be less true, I’m trying to figure out what are the right words to use… I’m not good at discounting, is that you have got to be friends with the government officials. But every now and then, the government officials turn against you and then they pick up your file and say, you did XYZ corrupting back in 1985. Sorry boys, you know, you’re in jail.

See, it’s a very messy system. Yeah, a lot of heartbreaks.

Professor Bruce Greenwald:

Okay, yes, go ahead.

Speaker #2:

Professor Bruce Greenwald:

Okay, for people who didn’t hear that question, the question was: as the fund has gotten bigger and has had almost of necessity to move into larger cap stocks, how has that changed the investment process?

Mr. Cheah Cheng Hye:

The investment process actually has not changed for us in response to size constraints or size considerations, I should say. It has changed in response to my intellectual frustration, with the notion that both in the Western world and the Eastern world, that successful, glamorous hedge funds depend on star managers or mysterious black boxes. I think I tried to describe how I tried to change it into a process of very ordinary manufacturing process, but the answer to your question is on several levels.

First of all, I think at some point, firms of Value Partners will come out against the constraints of capacity. Yeah, I think that’s the right word, capacity, yeah. We, in fact, briefly closed our funds several times in the past because we ran out of ideas. The way I have tried to do the job is that I know that at some point I won’t be able to take on any more money.

My self-interest is performance rather than size, because I earn performance fees, which are more important to me than the small annual fee I get for size, and I have responded.

If you look at my website from last year with my strategic partner, the Ping An Insurance Company of China, I launched an ETF division: Exchange-Traded Fund division. Three or four years ago, almost by accident I read the CFA journal, a professor from New York, but it is kind of unfair, I forgot his name. He was writing about the concept of fundamental indexing. He took the S&P 500, he picked the 25 cheapest stocks in terms of fundamental value, at least the lowest PE, if I am not mistaken, and it worked, he outperformed. I had simply copied his idea.

Okay, having succeeded with that, it was an astonishing example. I think I’ll blow my trumpet a little bit here, of a local Hong Kong Chinese firm being able to penetrate into a space dominated by 2 western multinationals; BlackRock and I think StateStreet.

We are not supposed to get in there. We got in there only because we came out of a differentiated product.

Now that we are successful, we are conceptually, and I will choose my words, because for regulatory reasons I cannot kind of say too much, but we are coming out with similar fundamental indexing products for other asset classes and markets across the Asian continent.

This will be my avenue for growth in future because of the limitations of the actively managed star.

Professor Bruce Greenwald:

In the back.

Speaker #3:

How does your research effort cover small and medium-sized companies in Asia, which are not covered by the institutional research community? To give you an example, IDS, which Li & Fung acquired a couple of weeks ago; it didn’t have any institutional research coverage on it at all, yeah. And if you just looked at it, you know that Victor and William Fung would support the company, and as part of that, when you have got somebody reputable like the Fung Brothers behind the company, do you give it a higher valuation, if you will, in terms of an asset allocation?

Professor Bruce Greenwald:

Oh, oh, there are two questions. The first is, how do you go about doing research on companies if there is no published research on those companies, except I assume the financials are available, so that’s the first question. The second question is, how important is the reputation for integrity and the quality of the people back in the companies, and how far does that affect your decision on the amount of money you’ll allocate to funds?

Mr. Cheah Cheng Hye:

Thank you for these questions. We are – you are talking with the right guy at this time because we are the pioneers of small-cap research and also China B-share research. The lack of published research is a huge advantage. You don’t really want someone else competing with you and researching the company. You want to be the first ambulance on the scene, you know, so I estimate that in my universe there are approximately 1000 to 1300 companies with market capitalization below US$1 billion.

I classify them as small cap stocks, and we have an army of people there researching them and confidently buying them, usually through structured deals; and these people are, frankly speaking, desperate. They don’t have a brand; they don’t have a major institutional investor as their shareholder, so we squeeze them. We usually ask, in one particular case I can still recall last year, we asked for the maximum discount of 19.9% to the quoted price in the stock market… And the guy said yes. Actually, I was astonished, but anyway I took it, you know.

So anyway, so no research is a good idea because it means you are really, really in the promised land, what I call Category #1. Remember I told you about Category 1, 2, 3? Yeah. Now, the real trouble with some of these guys are actually value traps. You could be in Category 1 forever. You never make any money out of it, you know? It refuses to move down the conveyor belt to category 2.5, when you are supposed to sell it, right? So, after you get in, it is fairly useful to try to encourage the management to do more IR and talk to the media and come out with this and that.

But, for your information, contrary to what some people in our audience may think today, in general, the accounting standards for Hong Kong listed companies is very high; it is world class. It is typically done by a Big-4 auditor.

We actually have the head of E&Y here, he used to work in Hong Kong for many years.

Anyhow, and the regulators are incredibly strict; they have a habit of jailing anyone who violates the securities regulations, so published accounts are not an issue, it is not some Mickey Mouse play at all.

Your second question is about integrity issues. This one is a tough one for me, too. I have been in the market – I am now 56 years old. I was a newspaperman from the age of 17 to 36, and from then on I was in the financial industry as a head of research, and then a money manager, and to this day I get fooled. I was fooled as recently as just a year ago by this guy who ran a company called Peace Mark who, however, was anything but peaceful.

He ran a chain of watch shops selling fancy European watches, and he disappeared after I had put in about Hong Kong $40 million into his company. We are still chasing him, and this guy is like the, I can’t remember the term now. I think it is something like the great grand wizard of the Freemason’s chapter of Hong Kong, a pillar of the community, the son of one of the most established colonial families, etcetera. So what do you do? That is why I told you, right? You have to be diversified, do a lot of background checks, and pray for the best.

奔驰受限三大内因 追赶宝马奥迪或无望

奔驰受限三大内因 追赶宝马奥迪或无望

2011年09月16日 03:40 来源:盖世汽车网 作者:Terry Miao

今年前几个月,奔驰以一种看似“无畏”的势头逆市而上,增势迅猛,动辄50%以上的同比增长率艳羡同行。但随着中国车市进入深度调整和竞争趋向白热化,奔驰因渠道混乱等问题最终没能hold住,销量增幅先后被宝马、奥迪超越,年中期间吵得沸沸扬扬的渠道整合也终归平寂,大家不禁要问,奔驰到底怎么了?

根据德系三大近几个月公布的在华销售数据,处于中国豪车市场金字塔顶端的奔驰、宝马、奥迪三大巨头处境却各有不同。进入7月份以来,宝马汽车增幅虽不再高歌猛进,但还能维持35%左右的增幅。奥迪汽车在改善了产能不足的顽疾之后,增速较前几个月有所上升,7月份在中国市场售车27455辆,实现了同比增长35%。具体来看,下滑最快的反而是此前增速最快的奔驰。继6月份“增速最快”这个名头被宝马夺去之后,7月奔驰在中国市场上更是出负增长,8月的增幅也仅仅只有3.2%。而且,在华一向倚重进口车的奔驰汽车上半年进口车的销量也出现了1%的下滑,61753辆的进口量同比不升反降,进口豪华汽车销量冠军的头衔被上半年进口量达82455辆,同比增幅达到50%的宝马给夺了去,奔驰只能屈居第二,奥迪则以同比增长53%至28166辆的业绩排名第三。

奔驰官方给出的解释是,其销量下滑主要归结为高产量的C级车更新换代所致。据其预测,第三季度在新C级车推出后整体销量将会反弹。但事实果真如此吗?业内普遍观点认为,奔驰在华混乱的销售渠道和一直无法提上去的国产化率以及对二三线市场的布局缺陷,才是导致其销量下滑的三大主要因素。

事实上,奔驰在华混乱的销售渠道一直以来都受到业界的诟病。目前,在中国市场上奔驰的三大销售主体分别为,北京奔驰、奔驰中国、利星行,但三者之间的利益关系始终纠缠不清。

作为一个经销商集团,利星行凭借其特殊的地位(占有奔驰中国49%的股份)导致不同阵营的经销商的待遇有着巨大差异。另外,主要负责销售进口奔驰汽车的奔驰中国和负责销售国产奔驰汽车的北京奔驰之间也为了各自的利益博弈不断,导致进口车和国产车销售各自为政,甚至互相掐架,由此产生了一个怪象:在2008年国产E级奔驰下线前夕,奔驰中国的经销商大幅降价甩卖进口的E级奔驰车,不仅挤占了国产E级奔驰的市场,更令其定价陷入被动,直接导致国产E级不得不跟随降价10万元之多,令北京奔驰利益严重受损,一身两头的“非主流”销售模式成了奔驰的阿喀琉斯之踵。

当然,企业的相关决策者已经认识到渠道整合的必要性,但要落实到执行层面又面临着诸多的问题,2011年7月,围绕奔驰在华销售权的整合,一部扑朔迷离的谍战片连续上演,匿名短信推动暗流涌动,从质疑整合到质疑领导个人能力,渠道整合遭遇巨大的无形阻力。北汽董事长徐和谊曾对此公开表示,有人在阻挠整合,但他同时也责定,奔驰的渠道整合一定要在年底前解决。可见,销售渠道的混乱已经严重制约了奔驰在华的进一步发展。

另一个方面,奔驰在华产品产能的规划布局也是其销量下滑的重要原因。奔驰一直以来都把进口车当做是其在华的主要业绩支柱,奉行的战略过于保守。奔驰在华的产能建设远远落后于两个德国同行,一味沉迷于进口奔驰的巨额利润,国产车型销量仅为整体的35%,而宝马和奥迪的这一数字则分别超过50%和85%。在产品区域布局上,奔驰的规划也在一定程度上钳制了其自身发展,与在三线城市布局超过20%份额的宝马相比,奔驰的这一比例还不足5%,其超出40%的销售店都集中在一线城市,而宝马把70%的精力放在潜力惊人的二三线市场。

中国正处于消费升级的渐进过程中,高端豪华车的需求是客观存在的,未来的豪车市场竞争必将愈演愈烈,奔驰在华不仅要同奥迪、宝马争抢市场份额,还必须做好迎接其他欧美日豪车品牌挑战的准备,因此,只有尽快解决好自身存在的问题,才能持续的领跑中国豪车市场。

2011年9月5日 星期一

美國消費難振 華靠內需自救

By Stephen S.Roach(史蒂芬‧羅奇) 耶魯大學教授、摩根士丹利公司(Morgan Stanley)亞洲非執行主席 2011-09-05

美國消費難振 華靠內需自救

0.2%——這是過去14個季度(2008年第一季度到2011年第二季度)以來,美國消費支出(經通貨膨脹調整)的每年平均增長率。自二戰結束以來,美國消費者從未在這麼長時間裏如此不濟。這數字精簡地解釋了美國以至全球經濟的問題所在。

這段前所未有的美國消費疲軟期可以分為兩個階段。從2008年第一季度到2009年第二季度,消費者需求連續6個季度下降,年降幅為2.2%。這波下降在大危機頂峰時最為慘烈毫不出奇,2008年第3和第四季度,消費支出下降了4.5%。

消費復甦疲弱 比想像中更差

2009年年中,美國經濟觸底,消費支出的變化也進入了第二階段——十分委靡的復甦。此後8個季度(2009年第三季度到2011年第二季度),每年平均消費支出增長率為2.1%。這是有紀錄以來最疲軟的消費復甦——比危機之前12年(1996至2007年)的平均增長3.6%,低整整1.5個百分點。

這些數字要比當初公布的低很多。作為7月發布的美國國民收入和產出帳戶(US National Income and Product Accounts)年度修訂工作的一部分,美國商務部統計學家將他們此前對消費支出的估計調低。由2008年初到2011年中,這14個季度的增長趨勢從0.5%調低至0.2%,向下修訂的原因主要來自一開始的6個季度——每年平均消費支出降幅被提高了一倍,從1.1%修正為2.2%。

我追蹤這些所謂的基準修訂已經40年了,到目前為止,這是我所見過的最大幅度調整之一。我們都知道,美國消費者的日子不好過,但如此幅度的修正表明,危機帶來的支出削減和隨後復甦的疲軟程度,遠低於人們此前的想像。

要看出背後的原因並不難,前所未有的地產泡沫,造成了創紀錄的信貸泡沫,借此東風,美國消費者多年來的支出均遠高於其支付能力。當兩個泡沫均以破滅收場時,過度消費的美國家庭別無選擇,只能削減開支,通過償還巨額債務和補充耗竭的儲蓄,來重建其受損的資產負債表。

經濟增長遜預期 美財赤勢增

然而,資產負債表的修復過程只是個開始。家庭部門債務佔可支配個人收入的比重,已從2007年高峰時的130%下降至2011年初的115%,但仍大大超過了1970至2000年間的75%平均水平。與此同時,個人儲蓄率從2005年年中的最低值——相當於1.5%的可支配收入——上升為2001年上半年的5%,但仍大大低於20世紀最後30年的8%平均水平。

削減開支和修復資產負債表還處在早期階段,因此美國消費支出半死不活的狀態還將持續。在過去兩年的疲軟復甦中,消費支出增長趨勢的2.1%,可能預視未來多年的普遍情況。

這樣的結果對經濟前景還將造成三點深遠影響:

首先,由於消費需求佔真實GDP的比重仍高達71%,消費趨勢的持續不振將對美國經濟增長蒙上一層陰影。已入歧途的華盛頓政客最喜歡的事情,莫過於讓消費者回到危險的消費老路上去,重新開始花錢消費,但過度消費的美國人現已清醒多了。試圖繞過資產負債表的修復,浪費了貨幣和財政刺激的彈藥。

其次,消費和GDP增長的持續疲軟,將嚴重影響美國的經濟增長,使之遠遠達不到政府長期預算估計時所依據的假設。國會預算辦公室假設,在2013至2016年間的真實GDP平均年增長率為3.4%。如果增長趨勢比這個數位低1個百分點——在消費持續不振的情況下,這可能性很大——財政赤字將顯著增加。

事實上,聯邦預算委員會的經驗表明,真實的GDP增長率若持續比預期的低1個百分點,相當於在10年的時間裏,增加大約3萬億美元的預算赤字。不消說,這樣一個結果,將大大激化已經莫衷一是的債務預算爭論。

激活消費信心 救美國救全球

最後,任何經濟體也無力填補美國消費持續不振所造成的需求缺口。歐洲和日本自不待言,而世界主要發展中經濟體,特別是中國也欠缺如此規模和動力。因此,美國消費的持續疲軟,意味着出口導向發展中經濟體將承受壓力。好消息是,這將迫使它們實施早就應該實施的「以刺激內需為目標」的再平衡戰略。

怎麼辦?危機高峰時所採取的措施——大規模財政和貨幣刺激——有助於讓自由落體平穩着陸,但對於有意義的復甦就不管用了。在修復資產負債表的時代,這一點都不令人奇怪。

相反,美國需要一系列政策,滿足消費者的需求和壓力。可行方案包括免除債務以加速去槓桿化過程;創造性儲蓄策略從而為受危機重創的美國人重建財務安全;當然還有增加收入和就業職位。

美國經濟——以及全球經濟——的復甦離不開美國消費者。現在,我們必須拋棄意識形態的藩籬——不管是左派還是右派——在政策爭論中弄清甚麼才是當務之急。(Copyright︰Project Syndicate 2011)

訂閱:

意見 (Atom)